The Futures Summit: A New Era of Development Cooperation

April 10, 2026 • 8:30 am – 4:30 pm EDT

Hosted by Global Development

Photo: Aleks Taurus/Adobe Stock

The United States is quietly losing access to the minerals that underpin its defense systems, semiconductor manufacturing, and reindustrialization agenda—not through geopolitical confrontation, but through commercial neglect. South Africa is the dominant U.S. supplier of platinum group metals, chromium, manganese, and military-grade vanadium, and no allied nation comes close to matching its combination of mineral wealth, processing capacity, and technical expertise. Yet rising energy costs and crumbling infrastructure are pushing South Africa’s processing sector toward closure, and without intervention, that capacity will continue migrating to China by default. As political tensions between Washington and Pretoria have intensified, it is worth remembering what is actually at stake: a supply relationship built over more than a century that would be extraordinarily costly to lose and nearly impossible to replace.

The United States and South Africa are navigating one of the most turbulent periods in their bilateral relationship. The Trump administration has been openly critical of South Africa’s Expropriation Act, and its foreign policy positions, including its case against Israel at the International Court of Justice and its continued engagement with Russia. In February 2025, the administration expelled South Africa’s ambassador and invited Afrikaners to resettle in the United States as refugees, framing them as victims of racial persecution. South Africa has pushed back firmly, rejecting what it describes as interference in its domestic affairs.

These tensions risk obscuring a commercial relationship that has served U.S. strategic interests for more than 100 years.

These tensions risk obscuring a commercial relationship that has served U.S. strategic interests for more than 100 years. Policymakers on both sides should avoid allowing diplomatic friction to undermine a minerals supply partnership that Washington would struggle to replace, as the only large-scale alternatives for many of these minerals are Russia and China—both foreign entities of concern.

Throughout this period, South Africa has remained an open and reliable supplier. It has historically maintained a more open minerals trade regime than most resource-rich countries, avoiding the broad raw mineral export bans seen in neighboring Namibia and Zimbabwe. At various moments in history, when the United States sought to reduce dependence on adversaries such as the Soviet Union or China, Washington deepened its minerals trade with South Africa. As a result, South Africa has consistently served as a dependable partner for minerals that underpin U.S. national, economic, and energy security.

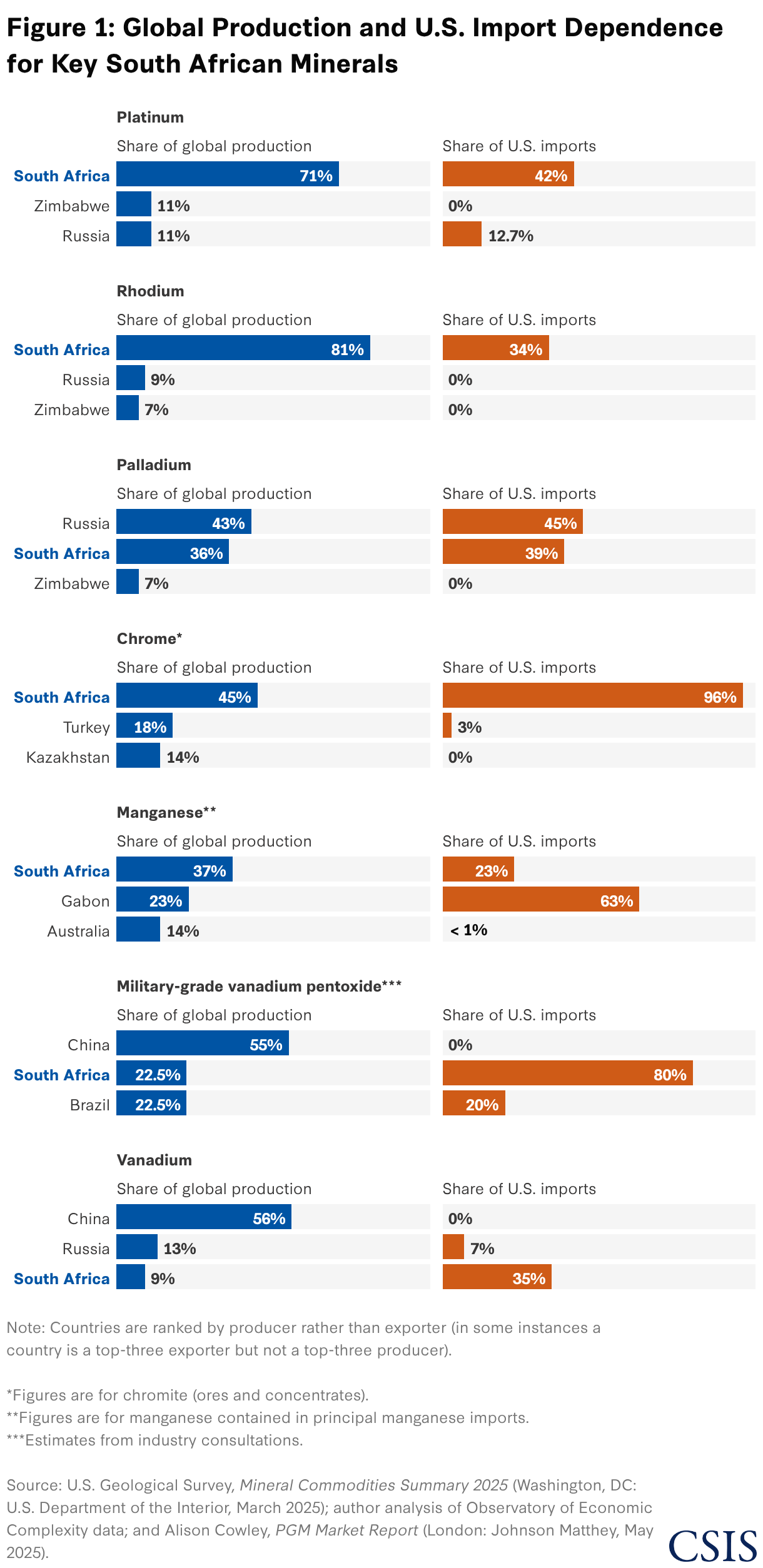

It is important not to lose sight of the foundation of the bilateral relationship: strong commercial ties and pragmatic economic cooperation. Today, South Africa is the United States’ largest supplier of platinum, rhodium, chromium, and military-grade vanadium, and is the second-largest supplier of manganese and palladium. South Africa was also one of the world’s top destinations for rare earth exploration in 2025, demonstrating its potential as a long-term supplier of these strategic materials to the United States. Few countries combine South Africa’s mineral endowment, processing capacity, and technical expertise. Preserving and strengthening this industrial base is therefore a strategic interest for the United States.

For many of the minerals covered in this brief, there is no allied alternative to South Africa. Diversifying away from South Africa would not mean diversifying toward Canada, Australia, or another partner nation—it would mean diversifying toward Russia and China. Russia is the world’s largest palladium producer and a significant platinum supplier. China dominates manganese processing and is rapidly expanding its position across the broader critical minerals supply chain. For chromium and military-grade vanadium, the supply base is even more concentrated: Outside of South Africa, there is effectively no Western-aligned source of scale. This is what makes the current moment so consequential. Every processing facility that closes in South Africa due to uncompetitive energy costs does not sit idle. It shifts activity to China. The question facing Washington is not whether to depend on a foreign supplier for these materials, but which foreign supplier that will be.

Every processing facility that closes in South Africa due to uncompetitive energy costs does not sit idle. It shifts activity to China.

South Africa sits atop one of the most extraordinary concentrations of mineral wealth on earth. The country holds the world’s largest-known reserves of platinum group metals (PGMs), chromium, and manganese, and ranks among the top globally for vanadium, titanium, zirconium, and fluorspar. South Africa’s ore reserves are valued at more than $2.5 trillion, with 16 commodities ranking among the top ten globally by reserve size. Critically, many of these minerals have no viable substitutes in their primary applications and are sourced by the United States overwhelmingly from South Africa. This resource endowment, combined with more than a century of accumulated mining and metallurgical expertise, makes South Africa uniquely positioned among U.S. partner nations to supply the critical minerals that underpin U.S. industrial, defense, and energy security

South Africa is the United States’ dominant supplier of platinum group metals, chromium, manganese, and military-grade vanadium—minerals that underpin U.S. defense systems, semiconductor manufacturing, automotive production, and any serious reindustrialization agenda. They have no viable allied alternatives: The next largest producers are foreign entities of concern, primarily Russia and China.

Palladium

Palladium is essential to semiconductor manufacturing, used in chip-to-board interconnections and protective plating that preserves performance and durability. The United States produces just 5 percent of global supply from two mines in Montana, both owned by South Africa’s Sibanye-Stillwater, and this production meets only about 16 percent of U.S. domestic consumption. The semiconductor industry is therefore heavily dependent on imports. South Africa is the world’s second-largest palladium producer after Russia, accounting for roughly 36 percent of global output. Anglo American’s Mogalakwena Mine alone contributes approximately 6 percent of global supply. This concentration makes South Africa a linchpin of the palladium supply chains underpinning U.S. semiconductor manufacturing.

Rhodium

In its 2025 assessment, the U.S. Geological Survey ranked rhodium as the second-most-critical mineral out of 60 evaluated. The United States is the world’s largest importer of rhodium. South Africa plays the leading role in meeting that demand, given that it is the biggest supplier of rhodium to the United States, accounting for 34 percent of U.S. imports in 2024, valued at approximately $643 million. This rhodium is vital for sustaining the domestic auto manufacturing industry.

Platinum

The United States is the largest offtaker of South African platinum, importing $2.9 billion worth in 2024, which represented 42 percent of total U.S. platinum imports. Russia was the second-largest supplier at $878 million, or 12.7 percent. Platinum is vital for a range of industries, including automotive manufacturing and hydrogen fuel cells. It is also used as an industrial catalyst in petroleum refining, fertilizer production, and pharmaceutical manufacturing.

Vanadium

Vanadium is critical for defense applications because it strengthens metals and improves performance under extreme conditions. Vanadium-strengthened steel is used in armored vehicles, submarine hulls, naval vessels, aircraft landing gear, and missile casings. It is also a key component in titanium alloys used in fighter aircraft, jet engines, helicopters, missile systems, and space technologies, due to their high strength-to-weight ratio and heat resistance. Beyond structural uses, vanadium is increasingly important for energy resilience through vanadium redox flow batteries, which provide long-duration energy storage for military bases and microgrids.

Of particular strategic importance is the military-grade form of vanadium pentoxide, which has no commercial-grade substitute in defense applications. It is a high-purity material, typically exceeding 99 percent purity. The United States relies on just two countries for this material: Brazil and South Africa. According to industry estimates, in 2025, only two mines supplied this material to the U.S. market—Largo in Brazil and Rhovan in South Africa. That year, South Africa accounted for 35 percent of U.S. imports of military-grade vanadium.1 By 2026, its share had risen to 80 percent, highlighting South Africa’s rapidly growing importance in this defense-critical supply chain.2

Chromium

Chromium is central to any serious U.S. reindustrialization agenda, as roughly 85 to 90 percent of global chromium consumption is used in stainless steel production for construction, infrastructure, industrial manufacturing, and energy systems. South Africa is the world’s largest producer of chromium, accounting for 44.7 percent of global output. The United States sources 96 percent of its chromium supply from South Africa, underscoring South Africa’s critical role in supporting U.S. industrial capacity.

Manganese

South Africa is the world’s largest producer of manganese, accounting for about 37 percent of global supply. It is also the second-largest supplier of manganese to the United States after Gabon, which has experienced political instability following a 2023 coup.

Like chromium, manganese is essential to U.S. reindustrialization. Its primary use is in steel production, where it strengthens steel and removes impurities during manufacturing. Beyond steelmaking, manganese is also becoming increasingly important in battery technologies, particularly lithium-ion batteries used in electric vehicles and energy storage systems. It is a key component in several battery chemistries, including nickel manganese cobalt oxide and lithium manganese oxide, where it helps improve stability while lowering costs relative to other materials.

Rare Earths

In 2025, South Africa received the sixth-largest amount of rare earth exploration globally—just one spot behind China and well ahead of jurisdictions such as Saudi Arabia and Greenland. This indicates strong investor confidence in South Africa’s long-term potential as a rare earth supplier. Exploration has already yielded good discoveries: At the Steenkampskraal deposit, the underground in situ average grade is approximately 14.5 percent run-of-mine, making it one of the highest-grade rare earth deposits in the world. In addition, surface tailings from earlier mining and processing operations remain stockpiled and contain about 7 percent total rare earth oxides (TREO). The Phalaborwa Rare Earths Project contains an estimated 35 million tons of ore with 0.44 percent TREO. As the United States builds out its rare earth processing capabilities for both light and heavy rare earths, the South African rare earths could be directed to the United States for separation and permanent magnet manufacturing.

South Africa’s mineral processing capabilities developed over more than a century, driven by successive waves of resource discovery, foreign investment, and deliberate industrial policy. Unlike many resource-rich countries that export raw materials, South Africa has decades of experience operating energy-intensive smelters, refineries, and metallurgical facilities, supported by a sophisticated mining ecosystem, engineering expertise, and research institutions such as the Council for Scientific and Industrial Research and Mintek.

Mineral processing capabilities were built on a foundation of gold. The discovery of the Witwatersrand reef in 1886 triggered one of the largest gold rushes in history and rapidly attracted British and European capital. To extract gold from the unusually deep and complex ore bodies, mining houses had to develop sophisticated processing and metallurgical techniques on site. The deep-level mining knowledge accumulated during this era became the bedrock of South Africa’s broader technical capabilities.

The discovery of the Bushveld Igneous Complex, which holds significant global platinum group metal, chromium, and vanadium reserves, expanded the processing challenge considerably. PGM refining is complex, involving multi-stage smelting, converting, and hydrometallurgical processes to separate platinum, palladium, rhodium, and other metals from one another. South Africa built this refining infrastructure domestically over the mid-twentieth century, partly because the Apartheid government, anticipating sanctions, made self-sufficiency in strategic industries an explicit national priority. Sasol’s coal-to-liquids technology and the development of domestic nuclear capability reflect the same impulse. The government set out to build it at home when sanctions threatened the ability to buy it abroad.

Mining companies played a central role in this era by vertically integrating from mine to refinery and investing heavily in proprietary processing technology. These companies built research divisions, trained engineers and metallurgists, and over generations accumulated institutional knowledge that is not easily replicated. Ferrochrome and manganese processing grew through a similar combination of resource proximity and industrial investment, with large smelting complexes built to serve both domestic steel production and export markets. Historically, South Africa has been one of the world’s leading ferrochrome producers precisely because it had both the ore and the processing infrastructure in the same place.

However, many of these industrial capabilities have eroded since the 2000s as energy costs rose, infrastructure deteriorated, and investment slowed. Processing that once happened in South Africa has gradually shifted to China, which offered cheaper electricity and aggressive industrial subsidies. While rebuilding that capacity is now a central policy challenge, the underlying technical knowledge, workforce expertise, and physical infrastructure have not disappeared entirely, which is why South Africa remains a more credible candidate for reindustrialization in minerals than most of its regional neighbors.

South Africa’s geographic position and infrastructure also make it a natural processing hub for the broader region. Although physical infrastructure has declined over time due to weak governance, the country has the most developed transport, financial, and industrial infrastructure in southern Africa, along with deep-water ports capable of handling large-scale mineral exports. It already functions as a commercial gateway for regional mining industries, including those in the Southern African Development Community, which hosts significant deposits of copper, cobalt, lithium, and rare earth elements. By expanding its processing capacity, South Africa could refine not only its own minerals but also materials produced across the region. This would reduce raw mineral exports to China while bolstering regional industrialization.

South Africa possesses one of the deepest pools of mining human capital in the world. The country has produced a generation of senior mining executives who now lead some of the world’s largest companies, including Newmont CEO Natascha Viljoen, Anglo American CEO Duncan Wanblad, Glencore CEO Gary Nagle, TechMet CEO Brian Menell, Vedanta CEO Deshnee Naidoo, Harmony Gold CEO Beyers Nel, and former Barrick CEO Mark Bristow. This leadership pipeline is supported by world-class mining engineering institutions such as the University of the Witwatersrand, the University of Johannesburg, and the University of Pretoria, which continue to train many of the engineers and technical leaders shaping the global mining sector. This depth of technical expertise, managerial talent, and institutional capacity provides a strong foundation for expanding downstream mineral processing and supporting the development of a regional processing hub capable of refining both domestic and regional mineral production.

In recent years, South Africa has faced enormous challenges with macroeconomic stability, financial sector integrity, and management of state-owned enterprises that have led to severe deficiencies in service delivery. However, since early 2024, the government has made notable progress in addressing some of these issues, contributing to improvements in the country’s investment climate.

Macroeconomic Reform: South Africa’s sovereign credit rating was downgraded to “junk” status by all three major agencies—S&P Global Ratings, Fitch Ratings, and Moody’s—between 2017 and 2020 amid weak economic growth, rising government debt, and political uncertainty. After several years of economic reforms, conditions began to improve. In November 2025, S&P Global Ratings upgraded South Africa’s long-term foreign and local currency sovereign credit ratings, marking the country’s first upgrade in nearly two decades. Standard Bank noted that the South African economy is now in its strongest position in a decade. Between May 2023 and March 2026, the South African rand appreciated by more than 18 percent, supported by economic reforms and strong gold prices.

Financial Grey Listing: In February 2023, the Financial Action Task Force (FATF) grey listed South Africa, indicating that the country had strategic deficiencies in its systems to combat money laundering and terrorist financing. Key concerns included weak enforcement of financial crime laws, limited prosecutions and convictions for money laundering, insufficient transparency around beneficial ownership of companies, and weak coordination among agencies responsible for investigating financial crimes. The grey listing had tangible consequences for South Africa’s financial system and business environment. International banks increased due diligence on transactions involving the country, and cross-border payments became slower and more expensive.

The FATF identified 22 action items that South Africa needed to complete to strengthen its financial integrity framework. In response, the South African government launched a whole-of-government reform effort involving the National Treasury, law enforcement agencies, and financial regulators. Measures included strengthening anti–money laundering legislation, expanding the powers of the Financial Intelligence Centre, increasing investigations and prosecutions for financial crimes, and improving oversight of high-risk sectors along with transparency around beneficial ownership. After completing the required reforms, The FATF conducted a thorough site assessment and removed South Africa from the grey list on October 24, 2025, following roughly 32 months of monitoring.

Despite these structural advantages and improvements, South Africa’s mining sector faces significant infrastructure and governance challenges that constrain its ability to realize this potential.

Industrial Decay: South Africa has a stronger mineral processing base than many resource producers, but it is uneven across commodities. The country’s most established processing ecosystem is in PGMs, where mining is supported by concentrators, smelters, base metals refineries, and precious metals refineries concentrated around the Bushveld Complex. Chromium is the second major pillar. South Africa remained the world’s leading producer of chromite ore in 2024, with output above 21 million tons, and its chromium value chain includes concentration and electric-arc-furnace smelting into ferrochrome for stainless steel. At the same time, South Africa’s chromium sector has become more upstream over time: It is now the largest exporter of chromium ore, even though it still accounts for a very large share of global ferrochrome output. That points to real processing capability, but also to slippage in downstream competitiveness.

South Africa is still a global leader in mineral processing capacity where legacy industrial infrastructure already exists, but it is losing ground in the most energy-intensive downstream segments. Increasing access to affordable energy will be crucial to ensuring these processing facilities stay operational in South Africa, as opposed to closing down and going to China.

The decay of many of South Africa’s industrial capabilities is a result of poor state-owned enterprise governance. In particular, Eskom (energy) and Transnet (rail and ports) have contributed to a decline in the country’s mining industry because they control the electricity and export logistics that underpin mineral production and processing.

Energy (Eskom): Mining is one of the largest industrial electricity consumers in South Africa, helping drive national power demand of roughly 219.6 terawatt hours annually. Chronic supply shortages and load-shedding have repeatedly disrupted mine output and smelting operations. During severe load-shedding cycles, analysts estimate platinum mine supply losses of 19–34 percent in South Africa, illustrating how electricity reliability directly constrains the country’s largest mineral exports.

The main weakness is that South Africa’s processing advantage has eroded where electricity is decisive. In ferrochrome, only 11 of 66 smelters were operating before the latest tariff relief, after electricity costs rose by roughly 900 percent since 2008. At the start of 2026, ferrochrome smelters were paying 135 cents per kilowatt hour (c/kwh). It has now been reduced to 87.74 c/kwh. Industry has stated they will need discounted power at a rate of 62 c/kWh, with the aim of lifting operating smelters to 45 by the end of 2026 and 49 by 2027. The Minerals Council South Africa has identified uncompetitive electricity prices as the primary constraint facing the country’s ferrochrome smelters. Cost comparisons illustrate the challenge: In 2024, the average production cost of ferrochrome was approximately $119 per ton compared with $103 per ton in China—a gap driven largely by higher electricity costs. Manganese is even more striking: Despite being one of the world’s largest manganese resource holders and a major ore exporter, South Africa has seen more than a dozen manganese smelters shut in recent years, leaving Transalloys as the last functioning manganese smelter by late 2025. Industry representatives have warned that without reliable and affordable power, mineral beneficiation does not present a viable business case in South Africa.

Eskom, which generates roughly 90 percent of the country’s electricity, has shown meaningful operational improvement after several years of severe power shortages that disrupted industry and mining production. In 2025–2026, the utility implemented a Generation Recovery Plan that improved the reliability of its aging coal fleet. The energy availability factor of Eskom’s power stations rose to roughly 69 percent in late 2025, reflecting improved maintenance and plant performance. As a result, South Africa experienced over 280 consecutive days without load-shedding, a significant improvement compared with 2022–2023, when rolling blackouts lasted up to 10 hours per day and constrained economic activity across the mining and industrial sectors.

Eskom’s financial position has also stabilized modestly, although it remains structurally fragile. The utility recorded a profit of approximately 16 billion ZAR in fiscal year 2025, its first annual profit in eight years, reversing a loss of about 55 billion ZAR the previous year. The turnaround was driven largely by government debt relief, electricity tariff increases, and reduced reliance on expensive diesel generators during periods of power shortages. The South African government has provided substantial fiscal support, including a multiyear debt relief package of roughly 230 billion ZAR, reflecting Eskom’s central role in the national economy.

Despite these improvements, Eskom continues to face significant structural challenges. Municipalities now owe the utility more than 110 billion ZAR in unpaid electricity bills, creating persistent pressure on Eskom’s balance sheet and cash flow. The long-term outlook remains uncertain because much of Eskom’s coal fleet is approaching retirement, with several plants expected to close beginning around 2029–2030, requiring large-scale investment in new generation and transmission infrastructure to maintain supply reliability.

Rail and Ports (Transnet): South Africa’s mineral economy depends heavily on Transnet’s freight rail and port network to move bulk commodities such as coal, iron ore, manganese, and chrome from inland mines to export terminals. Rail freight volumes have fallen sharply over the past decade—from about 226 million tons in 2017/18 to roughly 152 million tons in 2023/24—reflecting equipment shortages, theft, and infrastructure deterioration. Even after a modest recovery, rail throughput in 2025 reached only about 160 million tons, well below historic capacity. The logistics bottleneck has forced major exporters, including coal and iron ore producers, to curtail production when rail capacity cannot move sufficient volumes to port.

However, progress has been made. One of the most important reforms underway is the introduction of third-party access to the freight rail network, allowing private train operators to run on Transnet’s rail lines. The government has already shortlisted private companies to operate services on this network, a move expected to increase freight capacity and improve efficiency in transporting bulk commodities such as coal, iron ore, manganese, and chrome. The reform is projected to add around 20 million tons of additional freight capacity annually and represents a key step toward the government’s longer-term target of expanding rail throughput to roughly 250 million tons per year. Additionally, in October 2025, it was announced that Transnet is planning large-scale capital spend to modernize rail and port infrastructure. The company has announced plans to invest approximately $7.3 billion over the next five years to upgrade rail infrastructure, expand key export corridors, and modernize port facilities. Planned improvements include strengthening major mineral export routes and deploying new port equipment, such as container cranes at major terminals including Durban and Cape Town.

Together, Eskom’s power shortages and Transnet’s logistics constraints have become the two most binding infrastructure risks for South Africa’s mining sector—but they are slowly improving. Energy reliability determines whether mines and smelters can operate, while rail and port capacity determines whether mineral production can reach global markets.

The following recommendations offer a coherent strategy to preserve a supply relationship built over 150 years. Taken together, they address the three binding constraints on South Africa's mineral sector: energy, financing, and the bilateral framework needed to ensure that Western capital and offtake commitments reach South Africa before Chinese ones do.

Without stable and affordable electricity, many of South Africa’s mineral processing plants could face closure within months, forcing producers to export raw materials for processing abroad to China.

Reliable and cost-competitive baseload power is essential for energy-intensive industries such as mineral extraction and processing. While mining companies operating in South Africa strongly prefer to keep processing capacity in-country, many facilities cannot remain economically viable under current energy costs and supply constraints. Without stable and affordable electricity, many of South Africa’s mineral processing plants could face closure within months, forcing producers to export raw materials for processing abroad to China, further reinforcing China’s dominance in critical mineral supply chains. No allied nation offers a comparable combination of mineral reserves, existing processing infrastructure, and accumulated technical expertise. The United States has a direct interest in ensuring that base is not further eroded.

Invest in an energy corridor in Southern Africa. The United States should leverage the U.S. International Development Finance Corporation and the Export-Import Bank to support energy investments that crowd in private capital. The architecture for a regional energy corridor already exists through the Southern African Power Pool. Priority U.S. investments should focus on improving energy reliability, expanding transmission and distribution networks, reconductoring existing grid infrastructure, and developing diversified energy systems that combine LNG, renewables, and battery storage. Efforts should prioritize regions where mineral processing facilities require access to affordable and reliable power to remain viable, helping sustain domestic value addition and reducing the incentive to export raw materials to China for processing.

Investing in an energy corridor with the region would be deeply synergistic with U.S. mining interests, given its involvement across the region—Malawi has been a top destination of rare earth exploration, the United States has invested in Mozambique’s graphite and Zambia’s copper, and the United States is eyeing several projects in the Democratic Republic of Congo. Energy remains a structural challenge across the board. In December 2025, Australia’s South32 announced that it would be putting its Mozal aluminum smelter in Mozambique under care and maintenance by March 2026 due to difficult sourcing affordable and reliable energy from Eskom. CEO Graham Kerr noted that Eskom’s “only formal offer” for electricity supply was nearly $100 per megawatt-hour (MWh), while fewer than 1 percent of smelters outside China operate with contracts above $50 per MWh. South32’s Hillside smelter, the largest aluminum smelter in the southern hemisphere, has five years left on its current power contract. Without more affordable energy, this smelter, too, risks closure due to commercial viability challenges, undermining aluminum supply.

The South African Power Pool already provides a foundation for cross-border electricity trade and grid integration across the region. Established in 1995, the power pool links the national utilities of 12 Southern African countries through a shared transmission network and regional electricity market, allowing power to move across borders in response to supply and demand. The system already connects major generation sources—hydropower in Zambia and Mozambique, coal generation in South Africa, and emerging renewable capacity across the region—to industrial and mining hubs that depend on reliable electricity. Deepening U.S.-South Africa cooperation could significantly expand the generation and transmission capacity.

A useful starting point would be convening U.S. financing agencies, the South African government, development finance institutions, and the mining and energy industries to identify how partners can best work together to catalyze blended finance in support of this corridor and the mining projects within it.

Renew the U.S.-South Africa civil nuclear cooperation agreement. While the energy corridor should draw on a diverse mix of energy sources, strengthening nuclear cooperation should be an essential component. South Africa has a long-standing nuclear sector, and expanding it could provide a crucial source of baseload power to the region. South Africa has been the only country in the world to have a civil nuclear cooperation agreement with the United States under Section 123 of the U.S. Atomic Energy Act while maintaining uranium enrichment rights.

Although the Section 123 nuclear cooperation agreement between the United States and South Africa lapsed in 2022, discussions are ongoing to renew it. Advancing this would strengthen the framework for expanded nuclear collaboration between the two countries and provide greater certainty for U.S. firms, including for the deployment of U.S. nuclear technologies, potential reactor development, and expanded cooperation across the nuclear fuel supply chain.

Neighboring Namibia holds the world’s fourth-largest uranium reserves, accounting for roughly 8 percent of global resources. Namibia’s uranium sector is currently dominated by China. The China National Uranium Corporation, China General Nuclear Power Group, and the China Africa Development Fund hold significant ownership stakes in all three of Namibia’s operating uranium mines. As a result, roughly 77 percent of Namibia’s uranium exports are directed to China. Despite Namibia’s strategic importance in the global uranium supply chain and its strong economic ties with the United States, there is currently little meaningful U.S. investment in Namibia’s uranium sector. Expanding U.S. engagement across the nuclear fuel supply chain, from uranium production to fuel services and reactor technology, could strengthen regional energy security while deepening strategic economic ties across Southern Africa.

Southern Africa could also play an important role in strengthening U.S. energy security. The United States produces more nuclear power than any other country and operates the largest fleet of nuclear reactors in the world. Yet the fuel supply that underpins this leadership remains highly vulnerable. Despite efforts to diversify supply, the United States has historically relied heavily on Russian nuclear fuel services, creating a significant energy security vulnerability. Strengthening partnerships with uranium-producing regions such as Southern Africa could help diversify supply chains and support the long-term resilience of the U.S. nuclear sector. Southern Africa could be a crucial source of uranium to the United States in the long-term.

South Africa’s mineral wealth is not a future opportunity. It is a present strategic asset that the United States is already deeply dependent on, and that is quietly at risk. The infrastructure that mines, processes, and refines the materials underpinning U.S. defense, semiconductor manufacturing, and industrial capacity was built over more than a century and cannot be quickly reconstructed elsewhere. Washington and Pretoria are navigating a difficult diplomatic moment, but supply chain policy should not be held hostage to political friction. By pairing financing with offtake commitments, securing energy supply, and deepening bilateral cooperation, Washington can preserve a supply relationship that would be extraordinarily costly to lose—and that China is already positioning itself to absorb.

Washington can preserve a supply relationship that would be extraordinarily costly to lose—and that China is already positioning itself to absorb.

Beijing has not waited for Washington to act. Chinese firms have steadily expanded their presence across Southern Africa’s critical mineral supply chains through a combination of direct investment, offtake agreements, and infrastructure financing. In South Africa itself, Chinese companies have acquired stakes in manganese and chromium operations and are among the largest buyers of South African chrome ore, much of which is shipped to China for processing into ferrochrome that is then sold back to global markets. Across the broader region, China dominates Namibia’s uranium sector, holds significant positions in the Democratic Republic of Congo’s cobalt and copper mines, and has used infrastructure financing to build leverage over mineral export corridors. The pattern is consistent: China identifies a mineral it needs, finances the infrastructure required to extract and move it, secures long-term offtake, and processes it domestically. The risk to the United States is not that China might one day move into Southern Africa’s critical mineral supply chains. It already has.

Please consult the PDF for references.

Dr. Gracelin Baskaran is director of the Critical Minerals Security Program at the Center for Strategic and International Studies (CSIS) in Washington, DC.

This report is made possible by general support to CSIS. No direct sponsorship contributed to this report.

Commentary by Gracelin Baskaran — May 9, 2025

Critical Questions by Gracelin Baskaran and Meredith Schwartz — February 13, 2026

Critical Questions by Gracelin Baskaran — September 3, 2025