The Futures Summit: A New Era of Development Cooperation

April 10, 2026 • 8:30 am – 4:30 pm EDT

Hosted by Global Development

Photo: KTSDESIGN/SCIENCE PHOTO LIBRARY/Getty Images

America's economic security rests on its “exorbitant privilege” to borrow at low interest costs relative to the size of its debt, which sustains its economic and geopolitical strength. With the national debt at $38.77 trillion at the beginning of 2026, up 67 percent since 2020, and interest payments making up 12.1 percent of federal spending, sound management of this debt and the capital markets that fund it is of critical importance to U.S. resilience to economic and financial shocks. The persistent shift in issuance strategy to short-term Treasuries, starting under the previous administration and continuing in the current, risks limiting the government’s ability to respond to future shocks, clogging a vital artery of the financial system, and constraining monetary policy flexibility.

The U.S. Treasury’s principal objective in debt management is to “finance the government at the lowest cost over time”, which involves issuing debt across a range of maturities. T-bills, the shortest-maturity bonds, play a crucial role as a “shock absorber” of government borrowing. Maturing between just one month and one year, the price of T-bills is less sensitive to interest changes than longer maturity bonds, in other words, having a low duration. This makes T-bills an attractive safe-haven asset for investors to store cash on a short-term basis. This dash for T-bills in economic crises means that when the Treasury is in immediate need of a lot of cash, such as to fund emergency stimulus, a surge in T-bill issuance is the most effective way to keep the government liquid. However, although T-bills are price insensitive to rates, their yields—what the government pays in interest—are highly sensitive to short-term interest rate changes. Thus, their frequent refinancing exposes the government to volatile borrowing costs and investors to volatile returns over time, known as rollover risk.

This is seen in Figure 1, where the T-bill share of outstanding debt rises during recessions when governments must make fiscal interventions, and gradually declines during expansions as the Treasury returns to a more balanced maturity profile. This cycle maintains the Treasury’s ability to respond to crises like the 2008 financial crisis or the COVID-19 pandemic with countercyclical policy without oversaturating Treasury markets. In 2023, the T-bill share of debt surged in the absence of a recession, instead as a measure to keep the Treasury liquid after it drew down on its cash reserves when the United States temporarily hit its debt ceiling. While outside of a recession, the immediate need for cash necessitated compressing the T-bill “shock absorber”. The issue, however, has been the continued persistent reliance on T-bill issuance to finance the deficit.

It is tempting for the Treasury to continue using short-term bonds to finance the national debt. Treasuries remain the predominant global safe-haven asset, as no other country competes with the depth and liquidity of U.S. debt capital markets. However, the “convenience yield” of long-term Treasuries has declined in the face of increased U.S. economic policy uncertainty and fiscal imbalances. In other words, the premium global investors are willing to pay for long bonds’ safety and liquidity is falling. Conversely, T-bills carry a lower “term premium” than long-term debt as there is less risk to holding them over their short maturity, and are less reliant on foreign demand, with just 22 percent foreign ownership compared to 37 percent of longer-term Treasuries (see figure 2). While interest rates remain elevated, it is attractive for the Treasury to lean on T-bill issuance to keep borrowing costs low.

However, excessive and persistent T-bill issuance poses acute risks to government borrowing. The yield sensitivity to rate changes of T-bills creates rollover risk for the government. With debt being refinanced more frequently, the United States’ interest payments, already at all-time highs, become more sensitive to short-term changes in interest rates. Macroeconomic uncertainty stemming from countervailing trade, fiscal, and immigration policies complicates the Federal Reserve’s (Fed) interest rate path. Combined with a potential global energy crisis from conflict with Iran in the Persian Gulf, the potential for upside surprises to inflation and therefore interest rates could cause sudden, sharp rises in the U.S.’ borrowing costs.

The Treasury might point to how investors will always demand T-bills for their near-money status, always being attractive to park reserve cash and earn interest on a short-term basis. But it is precisely this substitutability that poses a serious threat to a crucial artery of the financial system.

The short maturity and market liquidity of T-bills mean that they are “near money”. Banks can easily liquidate them into cash if needed, but would rather earn their small interest essentially risk-free than hold cash that is eroded away by inflation. However, excessive T-bill issuance draws down on cash in the system, which reduces lending and seizes up key channels of financial activity. That forces the Fed to be a backstop and buy up what the private sector cannot, at the cost of its monetary independence, and creates a moral hazard for the Treasury.

The Secured Overnight Financing Rate (SOFR) is the interest rate for the shortest-term loans between financial institutions using Treasuries as collateral, otherwise known as repurchase agreements or “repo”. Although not directly set or targeted by the Fed, SOFR is the effective “market price of money” for over $3T in daily financing volume that feeds into the real economy. As a key short-term interest rate, the Fed works to prevent major deviations between SOFR and its Federal Funds Rate (FFR) target range to ensure effective monetary policy transmission. Under normal market conditions, the Fed achieves this by acting as a lender and borrower of last resort to financial institutions at the ceiling and floor of the FFR target range.

Excessive T-bill issuance disrupts repo markets by draining liquidity and seizing up lending. Banks buying up all the T-bills cost cash, while they must also meet minimum cash buffer regulations. When cash reserves fall too low, banks stop lending on repo markets to comply with reserve requirements. Yet demand to borrow cash does not fall and indeed grows with more T-bills as hedge funds in highly leveraged Treasury basis trades continually need to borrow to maintain their positions. With high demand for lending meeting little cash supply from banks, the SOFR spikes, causing a crucial lending artery of the financial system to tighten, and raising concern over the Fed’s ability to influence key interest rates. The Fed cannot credibly commit to its dual mandate without control over short-term interest rates, and as such has no choice but to intervene in Treasury markets. The Fed must absorb the Treasury’s excess debt issuance that markets cannot clear.

Multiple such episodes have occurred in recent history, most recently in December 2025 when the FOMC decided to reverse their balance sheet reduction of Treasury holdings from COVID (known as Quantitative Tightening). Accelerated T-bill issuance during the summer last year tightened liquidity and caused the SOFR spike above the FFR target range. In response, the Fed announced it would buy $40B of T-bills per month. These “reserve management purchases” (RMP) take T-bills off banks’ books and replace them with reserves. This allows banks to comply with cash buffer requirements, allowing repo lending to function as normal at “ample reserves” and keeping the SOFR within the FFR target range.

Just because the Fed stepped in and prevented a crisis does not change the problem: T-bill markets are so oversaturated that the Fed could not reduce its balance sheet below $6.5T before cash reserves in money markets were on the verge of drying up and needed intervention. Compare this to the $3.7T floor the Fed’s balance sheet hit before the September 2019 repo crisis, and it is evident that at current rates of T-bill issuance, the Fed must be not just a backstop, but an active participant in T-bill markets just to keep the financial plumbing going.

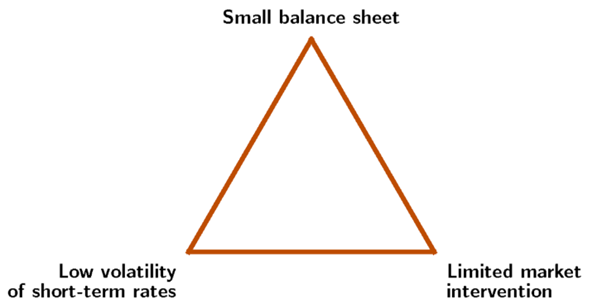

Economists of the Federal Reserve Board have presented a trilemma in central bank balance sheet management. At any time, a central bank can only choose two of three goals: low short-term interest rate volatility, limited market intervention, and a small balance sheet. The repo episodes encapsulate this: to maintain control over short-term interest rates like the SOFR, the Fed must either frequently intervene with operations like RMP or maintain a larger balance sheet.

Source: Burcu Duygan-Bump and Robert Jay Kahn (2026)

However, this trilemma only contains what is within the Fed’s control. These constraints may always be present, but excessive T-bill issuance only exacerbates them by further draining liquidity, needing more Fed involvement. This may very soon run into another hard constraint: Kevin Warsh, the nominee for Fed Chair, has made clear of his desire to significantly shrink the Fed’s balance sheet, which remains over 50 percent larger than pre-COVID levels.

In the face of continued large T-bill issuance, the Fed then must choose between frequent interventions or accept volatility in short-term interest rates. Given the Fed’s ultimate mandate of setting monetary policy in pursuit of price stability and maximum employment, it is unlikely that they will accept losing control of short-term interest rates. This leaves the Fed with no choice but to regularly intervene in markets.

The Treasury must not let this create a moral hazard. Price-sensitive private sector buyers are important to ensuring an efficient allocation of debt and reserves. When the Fed is an active market participant, price signals are distorted and do not discipline the Treasury’s borrowing. This encourages more borrowing, which can only be absorbed by the Fed. The Federal Reserve’s institutions are strong, but this risks creating the structural preconditions of “fiscal dominance”—where the Treasury’s borrowing needs take precedence over the Fed’s monetary policy goals: setting short-term interest rates and maintaining an optimally-sized balance sheet.

The Treasury must not become dependent on T-bill issuance for the United States’ daily financing needs. Not only does it expose the deficit to greater refinancing volatility, but it creates systemic risks that reduce the U.S. government’s ability to intervene when the economy needs it most. Continued T-bill issuance will tighten repo market liquidity, raising the risk of the financial plumbing seizing up. At the same time, it compresses the borrowing shock absorber before it is most needed to intervene in crises often precipitated by financial market failures. Relying more on the Fed will only serve to entrench moral hazard and further insulate the government from market discipline.

Policymakers would be well-advised to monitor stress in repo markets. As T-bill issuance continues, the “floor” of reserves needed to keep repo markets liquid will likely rise; keeping track of the floor will inform the Fed’s appetite to continue interventions like RMP as it potentially turns to further quantitative tightening. Returning issuance to a more balanced maturity profile, while temporarily painful by issuing more long-end debt that will raise yields somewhat, will reduce rollover risk, ease pressure on the financial plumbing, and give the Fed operational space to carry out its monetary policy as it sees fit. On its current path, the United States is running on a short duration of borrowed time.

For more analysis on how states interact in a transitioning global economy, check out our blog series, Charting Geoeconomics.